Learn when and how you should enroll in each of Medicare’s Parts

Medicare is a powerful program, which is why over 54 million American seniors have chosen it as their health insurance. Unfortunately, the program isn’t always the easiest to navigate—which results in thousands of Medicare beneficiaries paying late enrollment penalties and countless others choosing suboptimal plans that don’t quite fit their needs.

Use this guide to avoid costly mistakes, enroll on time, and choose the supplemental insurance that fits your specific needs. If you have questions or need assistance with Medicare, get in touch and we’d be happy to help!

Learn when to enroll in Medicare

While some Americans are eligible for Medicare due to disability, most become eligible for Medicare due to age. If you’re starting Medicare by way of turning 65, you’ll have a 7-month period to notify Social Security that you intend to enroll. This is your Initial Enrollment Period and it’s unique to your birth month.

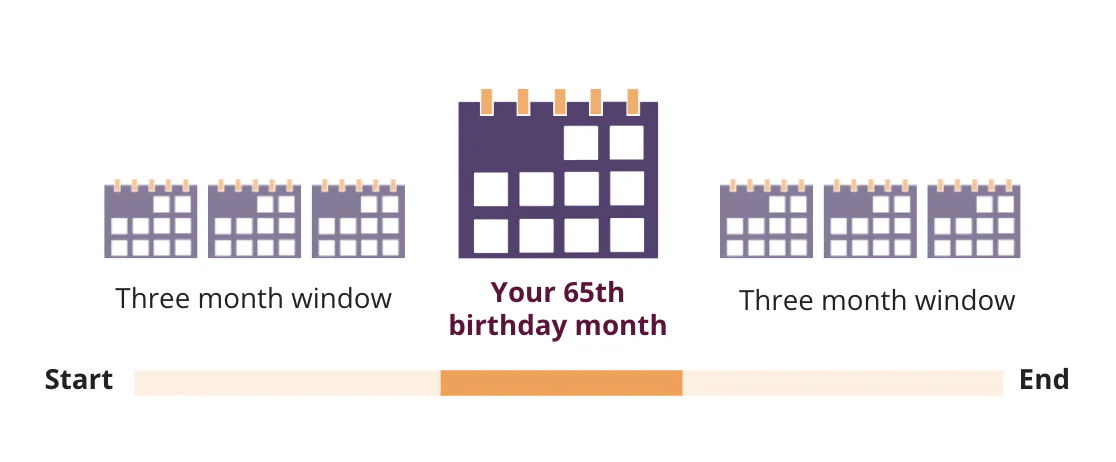

Your Initial Enrollment Period

You’ll use your Initial Enrollment Period to sign up for Original Medicare (Part A and Part B). Your Initial Enrollment Period begins 3 months before the month you turn 65, includes your birth month, and extends until 3 months after the month you turn 65. The only exception is if your birthday falls on the first day of the month. In this case, your Initial Enrollment Period shifts the 7-month window up by a full month (e.g., If your birthday is on February 1, your Initial Enrollment Period would start on October 1 of the year prior and extend to March 31—not April 30).

If you (or your spouse) are still working, you may prefer to keep your employer-linked insurance and delay your Part B enrollment. If you choose to do this, make sure you cover all of your bases. Check to see if you meet the eligibility requirements for the Part B Special Enrollment Period to avoid costly late enrollment penalties.

General Enrollment Period

What happens if you miss your Medicare Initial Enrollment Period? If you’re not eligible for a Special Enrollment Period, then you’ll be able to enroll during the Medicare General Enrollment Period, which occurs every year between January 1st and March 31st.

Wise Advice: If you enroll in Part B during the first General Enrollment Period after your Initial Enrollment Period, you will likely avoid the Part B late enrollment penalty.

When does Medicare coverage start?

If you sign up for Original Medicare during the first 3 months of your Initial Enrollment Period, your coverage will start on the first day of your birth month. If you sign up during your birth month or 3 months after your Initial Enrollment Period, your Medicare coverage will start the first day of the month following your enrollment.

It’s important to note that Original Medicare doesn’t cover everything. In fact, most notably, it only covers 80% of healthcare costs and doesn’t cover prescriptions. Once you’re enrolled in Original Medicare, you have the option to also enroll in supplemental coverage to cover what Original Medicare does not. This choice is incredibly important, and timing does matter, so pay close attention to this next section!

Choose your additional coverage

Original Medicare pays for 80% of covered services. The remaining 20% of medical costs can add up, especially if you have one or multiple health conditions—and Original Medicare also doesn’t cover prescriptions. That’s why Medicare introduced supplemental coverage options: Medicare Supplement (Medigap), Medicare Advantage (Part C), and Medicare Part D (prescription drug coverage).

Wise Advice: Your location, health needs, and financial situation will factor into your decision. So, don’t just ask your good friend, Dan, which option he chose!

Comparing supplemental insurance options isn’t easy. Most Medicare advisors will only share information about a few plans or carriers that they’re paid to represent. Medicare’s Plan Finder sounds helpful at first, but it has incomplete and incorrect information that can lead beneficiaries astray.

Chapter Advisors do things differently. They’re backed by Chapter’s tech platform that provides them with complete and accurate information for every option available to Medicare beneficiaries. They also get paid the same amount even if they recommend plans Chapter doesn’t get paid to represent. This helps you be sure that your advisor has your best interests at heart and will provide you with the best recommendation—bar none.

A summary of the differences

Medigap

Medicare Supplement (Medigap) plans sit on top of Original Medicare and help to cover the remaining 20% of costs not covered by Original Medicare. These plans are standardized and allow you to see any doctor who accepts Original Medicare. Many Medicare beneficiaries will pair a Medigap plan with a prescription drug (Part D) plan.

Medicare Advantage

Medicare Advantage, also known as Medicare Part C, is a bundled option that replaces your Medicare Part A and Part B (Original Medicare) coverage. By law, Medicare Advantage plans must cover at least the same services as Part A and Part B. They also generally provide additional benefits, including prescription drug coverage, dental, vision, and hearing coverage, and fitness programs. However, Medicare Advantage plans are not standardized, so before enrolling in one, understand the drawbacks and make sure your doctors and prescriptions are covered (we can help with that).

Part D

Medicare Part D covers prescription drugs, which are not covered by Original Medicare. While many Medicare Advantage plans come with prescription coverage, Part D plans are popular among Original Medicare and Medigap beneficiaries. Not enrolling in a plan with prescription drug coverage when you first become eligible for Medicare can result in costly penalties later on. So, even if you don’t have many or any prescriptions at this time, you should consider obtaining creditable prescription drug coverage.

Now that you have a general understanding of what each supplemental plan covers, it’s time to learn when to enroll.

Medigap (Medicare Supplement)

To enroll in a Medigap plan, you must have Original Medicare (both Part A and Part B). The best time to buy a Medigap policy is during your 6-month Medigap Open Enrollment Period because, during this time, insurance carriers cannot deny you coverage.

Your Medigap Open Enrollment Period

During the six months after you start Medicare Part B, you have a one-time opportunity to purchase a Medigap plan with no questions asked about your health history—and the carrier must cover all of your health conditions without charging you more. In other words, you are guaranteed issue because of your Open Enrollment right.

In four states—Connecticut, Maine, Massachusetts, and New York—Medicare beneficiaries 65 and older have guaranteed issue protections for Medigap plans regardless of when you purchase.

Wise Advice: Submit an application to have your Medigap coverage start on your Part B effective date to avoid gaps in coverage.

Purchasing Medigap outside of Open Enrollment

If you miss your Open Enrollment right and don’t live in one of the four states with guaranteed issue protections, you can still sign up for a Medigap plan if the insurer considers you “insurable.” They do this through medical underwriting, during which they ask you questions about things like your height and weight, health history, and medications.

Guaranteed Issue Periods

If you’re outside of your Medigap Open Enrollment Period, it’s worth checking to see if you qualify for Guaranteed Issue due to a Guaranteed Issue Period. The three common Guaranteed Issue Periods occur when:

You move out of a Medicare Advantage plan’s coverage area.

You have other health coverage that’s ending.

You tried a Medicare Advantage plan at age 65 and changed your mind within the first year. This is called a “trial right.”

Medicare Advantage

The best time to sign up for a Medicare Advantage plan is during your Initial Coverage Election Period, which occurs when you first start Medicare. For most people, this period is the same as their Initial Enrollment Period. Because you must have Original Medicare (Part A and Part B) to enroll in an Advantage plan, if you delay Part B enrollment, then your Initial Coverage Election Period will begin three months before your Part B effective date.

If you don’t sign up during your Initial Coverage Election Period, then you can sign up for a Medicare Advantage plan during the Open Enrollment Period that occurs each year between October 15th and December 7th. Those already enrolled in a Medicare Advantage plan may also choose to change their plan during this time.

Part D

When you initially enroll in Medicare, you’re also eligible to enroll in a Part D plan. For most people, this period is the same as their Initial Enrollment Period. If you sign up for Medicare outside of your Initial Enrollment Period, then your Initial Coverage Election Period for Part D will begin three months before your Part B coverage takes effect.

If you don’t sign up during your Initial Coverage Election Period, then just like with Medicare Advantage, you can sign up for a Part D plan during Medicare Open Enrollment (Oct 15 - Dec 7).

Review your plan options each year

Once you’ve finalized your coverage, you’re done, right? While you aren’t required to re-enroll in Medicare every year, you do have the option to change your plan each year. Why would you want to do that if you already picked the best option for your specific needs?

Medicare plans change each year. Some may remove doctors from their network, change prescription coverage, and remove benefits, while others may add benefits and services. The cost of plans also changes each year, and new plans may become available that suit your needs better than your previous plan. Plans may change, and so may your location or healthcare needs. For all these reasons, it’s important to shop around every year to be sure you’re on the plan that will give you the best value in the upcoming year.

Keeping track of enrollment periods and effective dates isn’t always easy, which is why we’re here to help! We’re happy to answer any questions you have and walk you through enrollment with as much assistance as you need. Grab some time to discuss your options here.