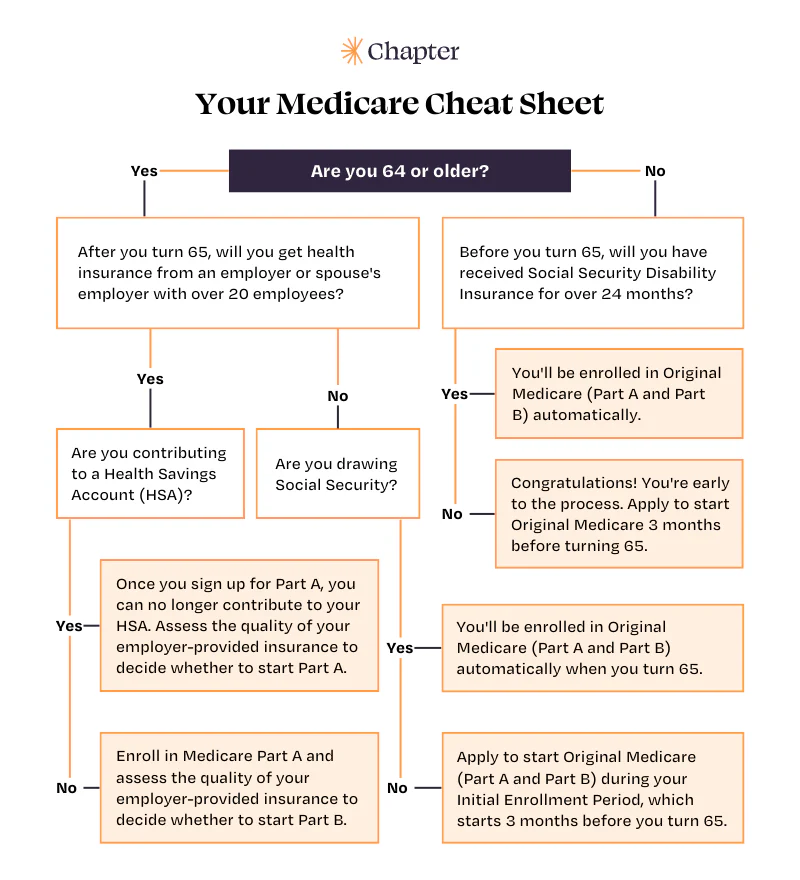

Most Americans become Medicare eligible when they turn 65—but if you (or your spouse) are over 65 and still have insurance through your employer, when should you enroll in Medicare? It depends on your situation, and there are a few key factors to consider:

Are you already drawing from Social Security?

If you’re already drawing from Social Security, then the Social Security Administration will assume you intend to enroll in Medicare and will automatically enroll you.

Are you receiving insurance from a small or large group employer?

If your employer has 19 employees or less, then it’s considered a small group employer. If you’re receiving insurance from a small group employer, you should enroll in both Part A and Part B to avoid a late enrollment penalty.

Are you contributing to an HSA?

If you’re contributing to an HSA, you need to either halt contributions or wait to enroll in any part of Medicare to avoid tax penalties.

Below, we outline specific scenarios to help you determine if you should enroll in Part A and Part B while continuing to work after 65. If you do enroll in both Part A and Part B while still working, you should also consider signing up for supplemental Medicare insurance at the same time to avoid enrollment limitations and penalties later on. If you have questions or want help with your Medicare decisions, don’t hesitate to get in contact with one of Chapter’s licensed Advisors—regardless of where you’re at on your Medicare journey.

If you’re 65 and drawing Social Security

If you’re already drawing Social Security income, then you will be enrolled in Original Medicare automatically. You should receive your red, white, and blue Medicare card a few months before you turn 65. Starting the month of your 65th birthday, your Part B premium will be deducted from your Social Security income.

Didn’t receive your red, white, and blue card? To confirm that you are enrolled in Medicare, view your status via your Medicare account or Social Security account online, or by calling the Social Security Administration. If you are not enrolled, contact social security to sign up during your Initial Enrollment Period.

If you’re waiting to draw Social Security and working part-time or with a small group employer

In this situation, you’ll generally want to enroll in Medicare during your Initial Enrollment Period. Because you are not yet drawing from Social Security, you’ll need to take action to sign up for Medicare.

Even if you want to remain on your employer-provided insurance, if you don’t enroll in Medicare, your insurer can refuse to pay the portion of claims that would have been covered by Medicare. Additionally, because you work for a small group employer, you could incur late enrollment penalties when you do choose to enroll in Medicare.

If you’re planning to continue to work for a large group employer with insurance and are not contributing to an HSA

Even if you plan to continue working for a large group employer, you should enroll in Medicare Part A (which is premium-free for most people) and assess the quality of your employer’s insurance to determine if you should enroll in Part B. This is because, oftentimes, Medicare provides better value than employer insurance. We’ll explain more about assessing your employer coverage below.

For now, if you plan to remain on your employer’s insurance, you should enroll in Part A and defer Part B enrollment until you stop working or lose your coverage. Just be sure you qualify for the Part B Special Enrollment Period! If you don’t plan to remain on your employer’s insurance, you should enroll in Medicare—including Original Medicare and supplemental coverage—to avoid penalties.

If you’re planning to continue to work for an active large group employer with insurance and are contributing to an HSA

If you’re contributing to an HSA, you should compare Medicare coverage to your employer coverage. If you intend to continue contributing to your HSA, then you shouldn’t sign up for any Part of Medicare because you will face a tax penalty. You must discontinue contributions to your HSA 6 months before you apply to enroll in Part A—but you can apply for Part A up to three months before you want it to begin.

Enrolling in Medicare Part D

Medicare Part D is a separate health plan for your prescription drug coverage. If you’re still working after 65 and decide to delay enrolling in Medicare, you need to pay careful attention to Part D.

Once you enroll in Medicare, after you stop receiving coverage from your employer plan, you should also enroll in Medicare prescription drug coverage—regardless of whether or not you take prescriptions regularly. This will help you avoid the Medicare Part D penalty later on.

If you don’t currently take prescriptions, you can just enroll in the lowest-cost plan. If your needs change, you can change your prescription drug coverage during Medicare’s annual Open Enrollment Period.

Qualifying for Special Enrollment Periods

Certain life events qualify you for a Special Enrollment Period. Other than working past 65, here are some situations where you can enroll or switch coverage during a Special Enrollment Period:

Moving back to the US after living abroad

Losing coverage from your spouse’s insurance

Enrolling or disenrolling in Medicaid

Moving out of the service area of a Medicare Advantage plan

If you don’t qualify for a Special Enrollment Period and miss your Initial Enrollment Period, you can enroll during the General Enrollment Period. However, you’ll likely have to pay a monthly penalty on top of your premiums if you sign up during the General Enrollment Period.

Comparing employer coverage to Medicare

More and more people are choosing to continue working after turning 65, and many of them are surprised to learn that Medicare provides better value than their employer-provided insurance. One reason for this is Medicare’s incredibly low annual deductible, which is only $257 (in 2025). For comparison, employer-provided insurance typically has deductibles that are at least $1,500 per year (and often far more).

When assessing your employer-provided coverage, you should consider:

How much your premiums are after your employer’s contributions

Whether or not you receive coverage for a spouse or dependent (there’s no Medicare family plan)

How much you like your coverage, including your deductible amount and out-of-pocket costs

If you want help determining if you should stay with your employer coverage or move to Medicare, we’re here for you! Pick a time to speak with one of our licensed Medicare Advisors, so you can feel confident in your decisions about Medicare.