Health Savings Accounts (HSAs) are a great savings tool. Your HSA contributions and expenses for qualified medical expenses are both tax free. HSAs are commonly used to pay for deductibles, coinsurance, and copayments.

There are two important things you need to know when it comes to HSAs and Medicare:

You cannot contribute to an HSA while you’re on Medicare, which is important to know when you first apply for Medicare

You can use your HSA to pay for Medicare expenses, including the Part B premium

In this guide, we’ll explain how to avoid penalties caused by contributing to an HSA while on Medicare, what you can use your HSA for while on Medicare, and more details on how HSAs and Medicare work together.

Key takeaways:

If you had an HSA before claiming Social Security benefits, you can use your HSA funds towards many Medicare-related expenses.

You shouldn’t enroll in Medicare if you’re still contributing to an HSA. You could face tax penalties if you do this.

You should stop contributions to your HSA six months before you apply to enroll in Medicare Part A.

What is an HSA?

A Health Savings Account (HSA) is a type of savings account that can be used for qualified medical expenses. HSAs are typically paired with high-deductible health plans. These types of health insurance plans have certain pros and cons. The drawback of high-deductible plans is that you’ll have to pay most of your medical expenses until you reach a relatively high deductible. HSAs can offset these costs.

HSAs can be used to pay for eligible medical expenses like over-the-counter (OTC products), glasses, and crutches or wheelchairs. Sometimes you can also use your HSA dollars on copays for doctor visits, prescription medications, and hospital fees.

If you enroll in Medicare coverage and you still have an HSA (but you aren’t contributing to it any longer), you can even use your HSA funds toward your monthly premiums. We’ll discuss this in more depth later on.

There are also many tax advantages with HSAs. The great thing about HSAs is that the money that you save in this account isn’t taxed and the goods and services you purchase are tax-free. Keep reading for more on this subject.

HSA and Medicare: What you can purchase

There are strict rules about when you can use your HSA upon enrolling in Medicare. But if you’re qualified to use your HSA, it can be very beneficial for Medicare expenses. You can use your HSA to:

Pay for Medicare Advantage monthly premiums

Any out-of-pocket costs like deductibles, copayments, and coinsurance for Medicare

Additional medical services that may not be covered including vision, dental, and hearing care

Services that may have more strict rules around coverage like chiropractic care and acupuncture

Home health services for custodial care

The only thing you can’t use it to pay for is your Medicare Supplement (Medigap) premium.

However, you should not enroll in Medicare if you’re still contributing to an HSA. If you’re drawing from Social Security and you contribute to an HSA, you could face tax penalties. We outline these consequences and how to avoid this situation in the next section.

Are you planning to enroll in Medicare and are currently contributing to an HSA?

Health savings accounts are a great way to pay for a portion of your healthcare costs. HSAs have a triple tax advantage:

Your contributions reduce your taxable income.

Any investment growth within the account is tax free.

Withdrawals for “qualified medical expenses” are tax free (we explain these more in the next section)

Why you shouldn’t enroll in Medicare while contributing to an HSA

Very important: Don’t start Medicare if you’re contributing to an HSA.

If you intend to continue contributing to a Health Savings Account, then you should not start any part of Medicare, because you will face a tax penalty. You must discontinue contributions six months before you apply to enroll in Part A. I’ve italicized the word apply because you can apply to enroll in Medicare up to three months before you want it to begin. If that’s the case, then you must discontinue your HSA contributions up to nine months in advance.

The application date is the key factor here, not when you start receiving Medicare.

For example, if you want your Medicare Part B to begin on January 1, 2024, and you notify Social Security in October, then you must discontinue making HSA contributions by March 31 because your Part A will be dated to April 1 even though your Medicare Part B will not start until January 1.

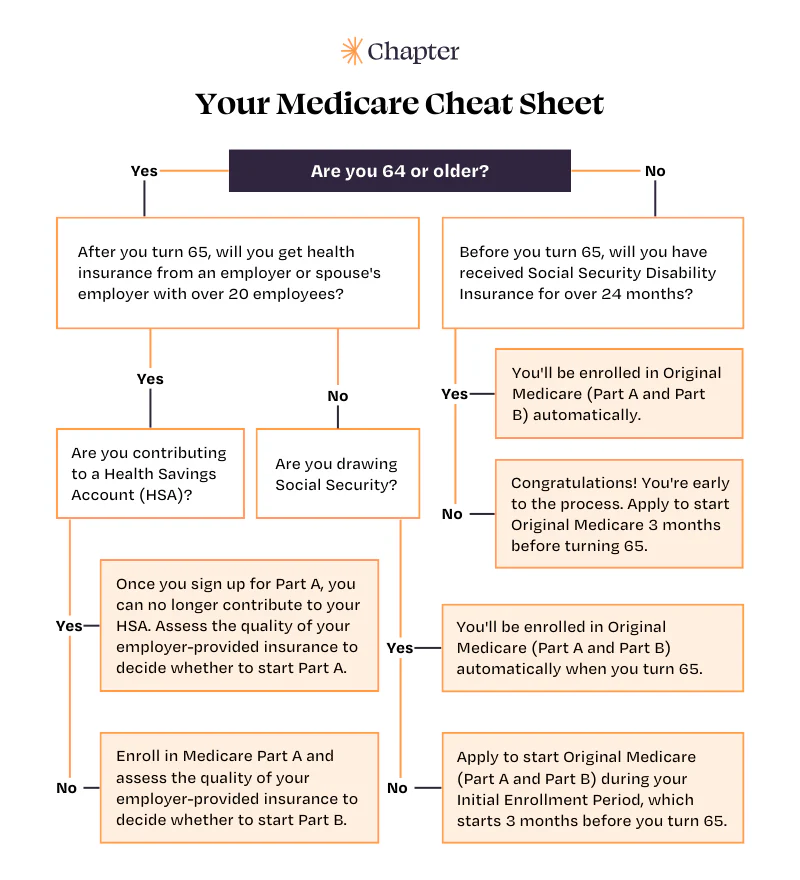

I’ve included a cheat sheet for Medicare enrollment from my book, It’s Not That Complicated below that can help you understand when to enroll in Medicare based on your specific situation, including your HSA contribution status.

Have more questions about your HSA and Medicare?

Keeping track of your dates for Medicare enrollment is confusing, especially when factoring in HSA contributions. Focus on living out the best next Chapter of your life, and leave the Medicare process to us. If you have questions about when you should stop your HSA contributions, when you should enroll in Medicare, or how you can use your HSA to pay for Medicare-related expenses, we’re here to help!

Schedule a free consultation or call us at (855) 900-2427 to get your questions answered and feel confident in your Medicare decisions.