Medicare Supplement Plan G (also called Medigap Plan G) is often considered the best Medicare plan. If it's "the best," why isn't everyone signing up for Medicare Plan G? Like with all health insurance plans, it's not perfect. In this article, we'll share all of the wonderful positive elements of Plan G, but we'll also share the drawbacks. Many of these pros and cons are common among all Medicare Supplement plans, so it's important to understand how Medicare Supplement plans work in general. That said, we'll indicate how Medicare Supplement Plan G has unique advantages.

Key takeaways:

Medicare Supplement Plan G reduces your out-of-pocket costs, giving you financial predictability.

Medicare Supplement Plan G gives you great access to care through no networks and no prior authorization requirements.

Medicare Supplement Plan G does have higher premiums than some Medicare Advantage plans and some of the other Medicare Supplement plans.

Medicare Supplement Plan G doesn't provide prescription drug coverage or extra benefits that often come with Medicare Advantage plans.

Enrolling in a Medicare Supplement Plan G can pose challenges if you try to enroll outside of a guaranteed issue period.

A brief overview of Medicare Supplement Plan G

Medicare Supplement Plan G is one of ten standard Medicare Supplement plans. Medicare Supplement plans are also commonly referred to as Medigap plans. So, Medicare Supplement Plan G and Medigap Plan G are the same thing. It's also worth noting that every Plan G has identical coverage, regardless of the insurance company that offers it or the monthly premium. All Medicare Supplement plans stack on top of Original Medicare to help cover the 20% of costs not covered by Original Medicare. This is different from Medicare Advantage, which replaces Original Medicare.

>> Learn about the pros and cons of Medicare Supplement vs Medicare Advantage

If you have Original Medicare and Medicare Supplement Plan G, you have the most comprehensive medical coverage you can get. That's because Medicare Supplement Plan G covers almost all of your out-of-pocket costs. Your Medicare Part B deductible is the only exception. That means that once you meet your Part B deductible, which is $283 in 2026, you'll owe nothing else out of pocket for the medical services you receive. Need a surgery that costs $600,000? You'll owe nothing. Especially since we generally need more medical services as we age, this makes Plan G a fantastic deal in the long run.

Note: Medicare Supplement Plan F does cover the Part B deductible, making it more comprehensive. But those who turn 65 after January 1, 2020, are unable to enroll in Plan F.

What does Medicare Supplement Plan G cover?

Plan G covers nearly every gap that Original Medicare leaves behind. Here's what's included once you've met your annual Part B deductible:

Part A hospital coinsurance: including up to 365 extra days of inpatient care after Medicare benefits are used up

Part A deductible: $1,736 per benefit period in 2026, which can apply more than once in a year

Part B coinsurance: the 20% of approved costs for doctor visits, outpatient services, and lab tests

Part B excess charges: what doctors who don't accept Medicare assignment can charge above the Medicare-approved amount (Plan N does not cover this)

Skilled nursing facility coinsurance

Hospice care coinsurance

First three pints of blood per calendar year

Foreign travel emergency care: 80% of medically necessary emergency care outside the U.S. after a $250 deductible, up to a $50,000 lifetime limit

The one gap Plan G does not fill is the annual Part B deductible of $283 in 2026.

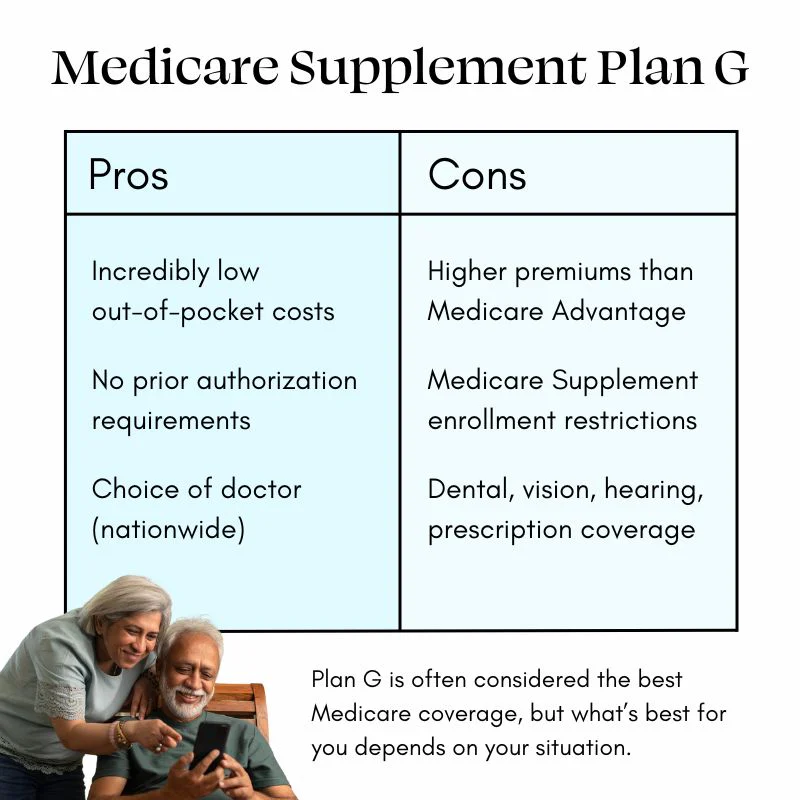

The pros of Medicare Supplement Plan G

All Medicare Supplement plans share some common advantages. In the following sections, we'll indicate which advantages are and are not unique to Medicare Supplement Plan G. If you review the chart below, you'll see that the only out-of-pocket cost that Plan G does not cover is the Part B deductible.

Incredibly low out-of-pocket costs

All Medicare Supplement plans reduce out-of-pocket costs. That said, Plan G reduces them the most. Outside of Plan F, which isn't an option for most new Medicare enrollees, Medicare's Plan G covers the most out-of-pocket costs. Medicare Supplement Plan N comes close to Plan G and is a good option for many. The only difference between Plan G and Plan N is that Plan N doesn't cover Part B excess charges, which don't apply in some states.

The only advantage that's totally unique to Medicare Supplement Plan G is having virtually zero out-of-pocket costs. This advantage should not be underestimated! Once you meet your annual Part B deductible of $283 in 2026, which is low for health insurance, you will have no other out-of-pocket costs for the year. This enables you to go to the doctor and get the care you need without financial fear. There's no reason to put a surgery off or skip an appointment because you won't owe anything. You'll also be able to know exactly how much you'll pay each year for healthcare because your out-of-pocket costs are so limited.

It's also worth highlighting one of the most valuable things Plan G covers that's easy to overlook: the Part A hospital deductible. At $1,736 per benefit period in 2026, this deductible can hit more than once in a year if you have multiple hospital stays. Plan G covers it entirely.

No prior authorization requirements

If you're on Original Medicare, regardless of additional coverage, then you won't have Medicare prior authorization requirements. So, this "pro" applies to people who are on Original Medicare, whether or not they have a Medicare Supplement plan.

Choice of doctor (nationwide)

Like with prior authorization requirements, if you're on Original Medicare, regardless of additional coverage, you can see any doctor who accepts Medicare nationwide. This is great because over 90% of doctors nationwide accept Medicare. Particularly if you travel a lot domestically or split time between two states, this is a critical advantage that allows you to receive timely care. Many people also like that this gives them control over seeing the best specialists in the nation rather than one that's in their plan's network.

The cons of Medicare Supplement Plan G

No health insurance plan is perfect, and all of them have their own pros and cons. Particularly when comparing Medicare Supplement Plan G to Medicare Advantage plans, there are a few drawbacks to address.

Higher premiums

For the coverage you receive, the premiums are generally worth it when compared against Medicare Advantage plans and the other Medicare Supplement plans. That said, Medicare Plan G premiums are higher than those for many Medicare Advantage and Medicare Supplement plan options. Monthly premiums for Plan G typically range from around $100 to $200+ per month depending on your location, age, gender, and tobacco use. In fact, many Medicare Advantage plans have zero-dollar premiums (keep in mind that you still need to pay your Part B premium of $202.90 in 2026).

Medicare Supplement enrollment restrictions

Medicare Plan G premiums may not seem worth it if you're healthy, don't visit the doctor a lot, and don't need a lot of medical care. Unfortunately, however, you cannot enroll in a Medicare Supplement plan when it makes sense for you. Medicare Supplement plans have enrollment restrictions. When you first enroll in Medicare, you are guaranteed acceptance into any Medicare Supplement plan. Outside of this time (and a handful of guaranteed issue periods), you'll likely need to undergo medical underwriting. With medical underwriting, insurance carriers can deny your application or charge you more based on your answers and health history. Unfortunately, due to enrollment restrictions, some people are unable to enroll in a Medicare Supplement Plan G when they decide they want to.

No dental, vision, hearing, or prescription coverage

One of the biggest advantages of Medicare Advantage plans is they provide extra benefits, like coverage for prescriptions and dental, vision, and hearing services. If you're on Original Medicare, whether you have a Medicare Supplement plan or not, you'll need to enroll in a standalone Part D plan to get your prescriptions covered. You also won't receive coverage for dental, vision, and hearing services. That said, the average cost of Part D coverage is $45. Also, in many cases, the value of the dental, vision, and hearing coverage that comes with Medicare Advantage plans is not very high.

What about High-Deductible Plan G?

Plan G also comes in a high-deductible version, sometimes called HD Plan G, that's worth knowing about. High-Deductible Plan G has the same coverage as standard Plan G, but you pay all Medicare-approved costs out of pocket until you reach a deductible of $2,950 in 2026. Once you hit that threshold, the plan kicks in and covers everything standard Plan G would cover for the rest of the year.

The tradeoff is significantly lower monthly premiums, often $40 to $80 per month compared to $100 to $200+ for standard Plan G. This makes High-Deductible Plan G a popular option for people who are relatively healthy, don't visit the doctor often, and want protection against a catastrophic medical event without paying high premiums every month.

The catch is the same as with standard Plan G: once you're past your initial Medigap Open Enrollment Period, you'll likely have to answer health questions to switch plans. So if you start on High-Deductible Plan G and later want to move to standard Plan G, you may not be able to. It's a long-term decision worth discussing with a licensed Medicare Advisor.

Frequently asked questions

Is Medicare Plan G worth it?

For most people who use their healthcare regularly, yes. Once you pay the $283 Part B deductible in 2026, you owe nothing out of pocket for covered services for the rest of the year. For people who have surgeries, chronic conditions, or frequent specialist visits, the math usually works strongly in Plan G's favor, even accounting for the higher monthly premium.

What does Plan G not cover?

Plan G does not cover the annual Part B deductible ($283 in 2026), prescription drugs (you'll need a standalone Part D plan), or dental, vision, and hearing services. It also doesn't cover services that Original Medicare itself doesn't cover.

What's the difference between Plan G and Plan N?

Both are strong options, but Plan G covers Part B excess charges. Plan N does not. In states where excess charges are common, or if you see specialists frequently, Plan G offers broader protection. Plan N typically has lower premiums in exchange for that trade-off. You can read a full comparison of Plan G vs. Plan N here.

What's the difference between Plan G and Plan F?

Plan F covers the Part B deductible; Plan G does not. That's the only coverage difference. However, Plan F is only available to people who became eligible for Medicare before January 1, 2020. If you turned 65 on or after that date, Plan G is the most comprehensive Medigap plan available to you.

When is the best time to enroll in Plan G?

The best time is during your Medigap Open Enrollment Period, the six-month window that starts the first day of the month you turn 65 and are enrolled in Part B. During this window, you cannot be denied coverage or charged more based on health conditions. After this window closes, insurers can require medical underwriting and may deny your application.

How to decide if Medicare Supplement Plan G is right for you

Everyone's situation is different. You'll have different budget and medical needs than your next door neighbor, and even your spouse! We always recommend working with an independent Medicare agent to understand and compare all of your options. A Chapter Medicare Advisor can help you do just this. Get started today by giving us a call at 855-900-2427 or picking a time to talk today.

Sources

Medicare.gov. (2026). Compare Medigap Plan Benefits. https://www.medicare.gov/health-drug-plans/medigap/basics/compare-plan-benefits

This article was last updated on March 13, 2026